Working capital is the lifeblood of any business as it meets day-to-day operating expenses. However, it is often noticed that small businesses in India face the biggest challenge of maintaining sufficient cash flow for working capital requirements. The challenge is mainly related to managing receivables and payables meticulously to maintain a comfortable liquidity position. However, delayed payments or short payment terms often lead to shortages in liquidity. Small businesses are affected the most facing missed opportunities.

Supply chain financing (SCF) addresses these issues to the advantage of suppliers, buyers, and lenders. Traditional lenders like banks have forayed into the space, but in reality, they are reluctant to extend financing to new and small businesses in smaller cities due to concerns of credit risk, insufficient knowledge about the company’s business model, and the relatively higher cost of servicing small loans. This is because such firms lack the credentials and credit history necessary to obtain traditional funding. It is estimated that nearly 50% of the working capital demand in India comes from Tier 2 and Tier 3 cities in Gujarat, Maharashtra, and Uttar Pradesh while Tier 1 cities in states like Karnataka, Maharashtra, Tamil Nadu, and Telangana generate about 25% of the demand.

To solve the challenges faced by both enterprises and traditional lenders, mid-market enterprises are increasingly relying on non-banking financial companies (NBFCs) for SCF because they offer more flexible and customized financing solutions, possess a deeper understanding of the supply chain, and are more responsive to the customized needs of these enterprises.

In India, there are two distinct approaches to SCF :

This focuses on leveraging accounts receivable as a means of obtaining financing. It involves using outstanding invoices or trade receivables as collateral to access immediate cash flow. This form of financing allows businesses to sell their unpaid invoices to a financial institution (or a factor) at a discounted value.

This method works on providing credit facilities against the current assets being financed. They are provided by financial institutions and are typically structured as revolving lines of credit both on the account receivable as well as account payable side.

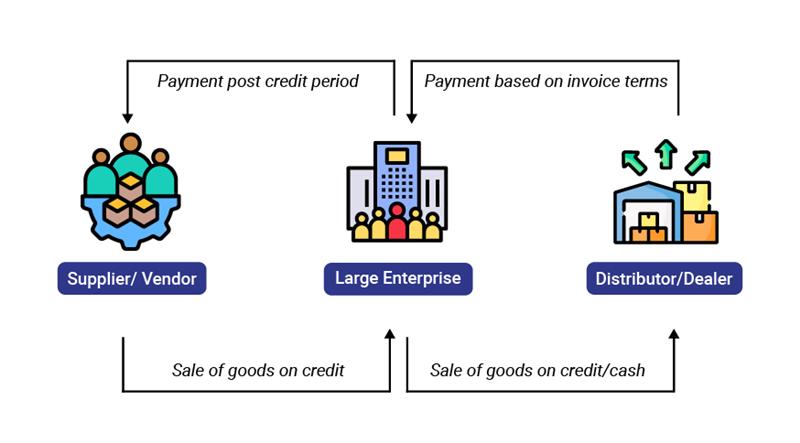

This ensures prompt payment for the vendors (suppliers to anchor). The anchor agrees to approve invoices for early payment by a third-party financier, who then advances the funds to the vendor. The full amount of the invoice is paid to the financier by the anchor on the due date. The programs include Sales bill discounting, Purchase order financing, Pre-shipment financing, Vendor Sales Factoring.

This enables dealers to avail of extended credit periods to finance their purchases from anchors and boost their sales. This provides the dealer with flexibility in managing their payment obligations. The programs include Purchase Bill discounting, Sales Factoring, Revolving limits / loans.

The evolving technology landscape, improved data accessibility, and enhanced transparency in trade transactions are reshaping the landscape of SCF. Thanks to initiatives including the introduction of platforms like Trade Receivables Discounting System (TReDS), which streamlined the financing and discounting of trade receivables via multiple financiers, and the implementation of Account Aggregator framework, which facilitated suppliers and buyers in accessing various financing options in a secure and seamless manner. These apart, advancements in technology, such as blockchain, data analytics, and digital platforms, are revolutionizing supply chain finance and facilitating the following benefits to borrowers

The views in this blog are those of the author and do not necessarily reflect the views of Vivriti. This article is for general information only and is not legal or investment advice.

The views provided in this blog are those of the author and do not necessarily reflect the views of Vivriti. This article is intended for general information only and does not constitute legal or investment advice.

Copyright © 2023 Vivriti Capital. All Rights Reserved

Under Construction

Please fill in the details

to cancel the NACH mandate

Please fill in the details to cancel the NACH mandate

Ms Namrata Kaul brings on board over 30 years of global banking experience. She has served as the Managing Director, Corporate and Investment Banking at Deutsche Bank AG. Prior to that she was Head of Asia Business for Deutsche Bank based out of London, involved in multi country interface. Ms Kaul has been involved in developing the strategy roadmap for Deutsche Bank India as part of the India Board and was instrumental in defining and executing the Asia Focus strategy for the EMEA business. She was the founder of Deutsche Bank's Diversity initiative in India. Ms Kaul had earlier worked with ANZ Grindlays Bank in various leadership roles across Treasury, Corporate Banking, Debt Capital Market and Corporate Finance in India and the UK.

Ms Kaul serves on the Board of CARE International. She is a Management Postgraduate from IIM Ahmedabad and has completed a Chevening scholarship on Leadership from London School of Economics.