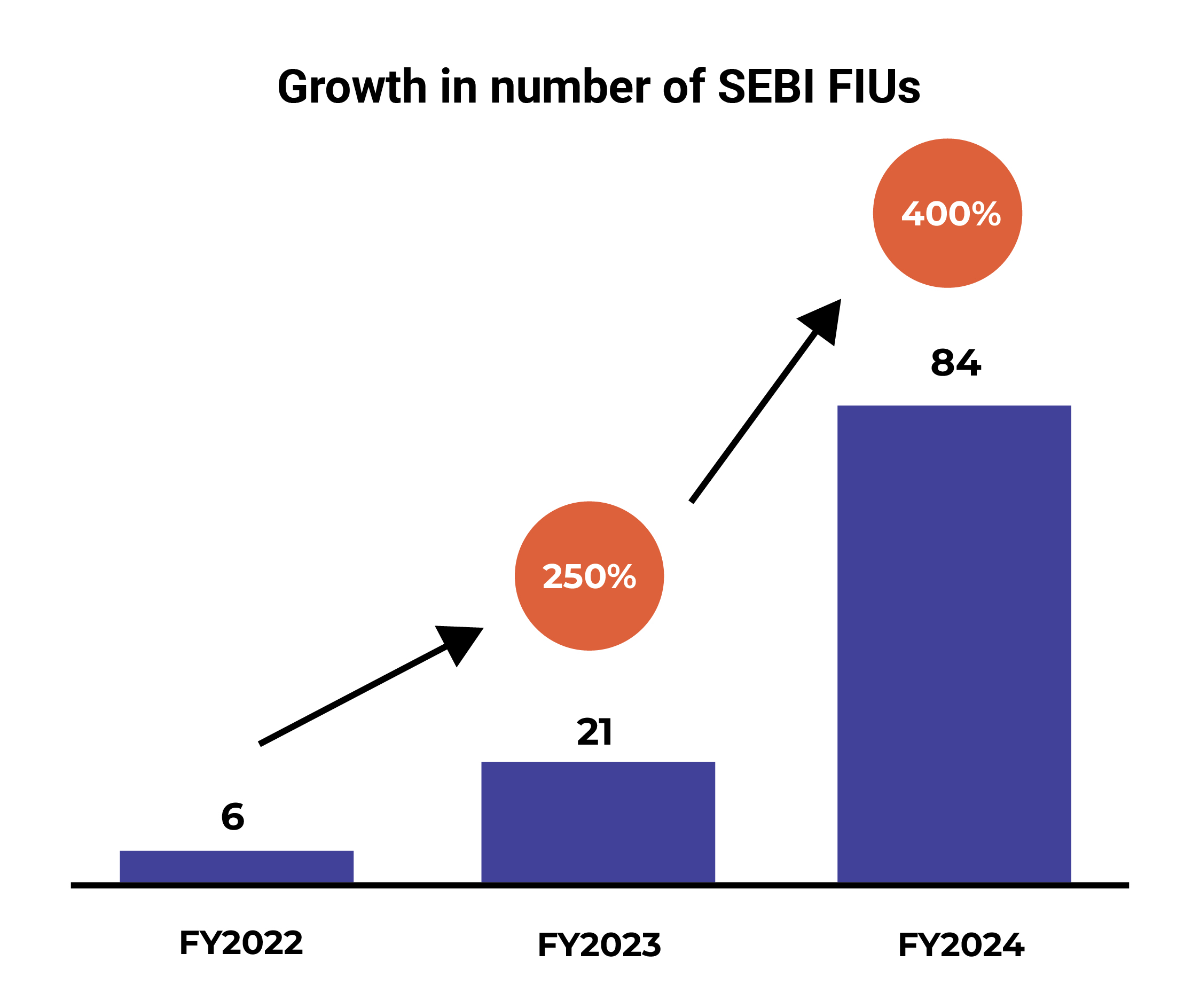

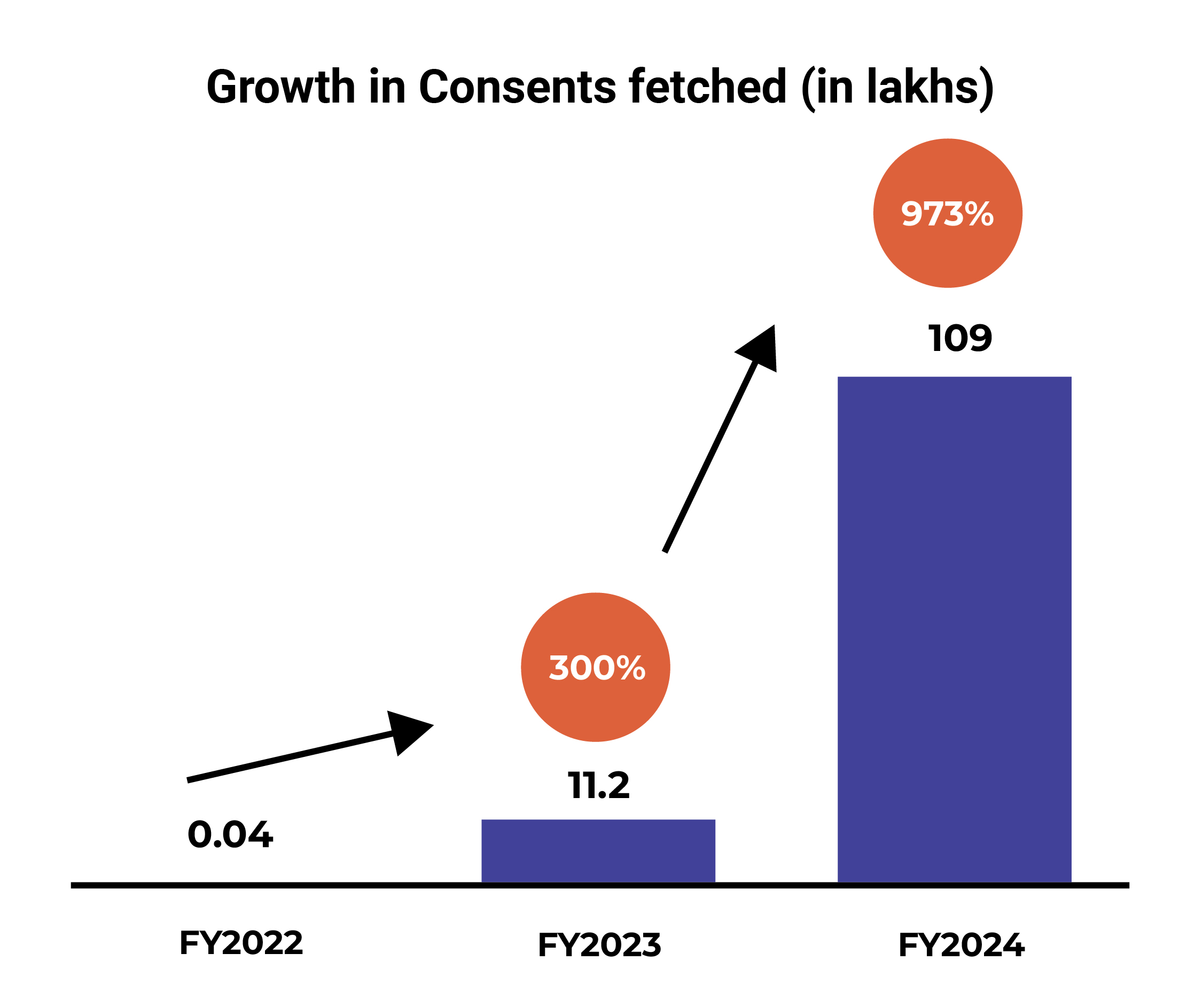

“Lending firms using the Account Aggregator (AA) framework facilitated loans worth INR 42,300 crore during the period of September 2021 to March 2024.”

– Sahamati

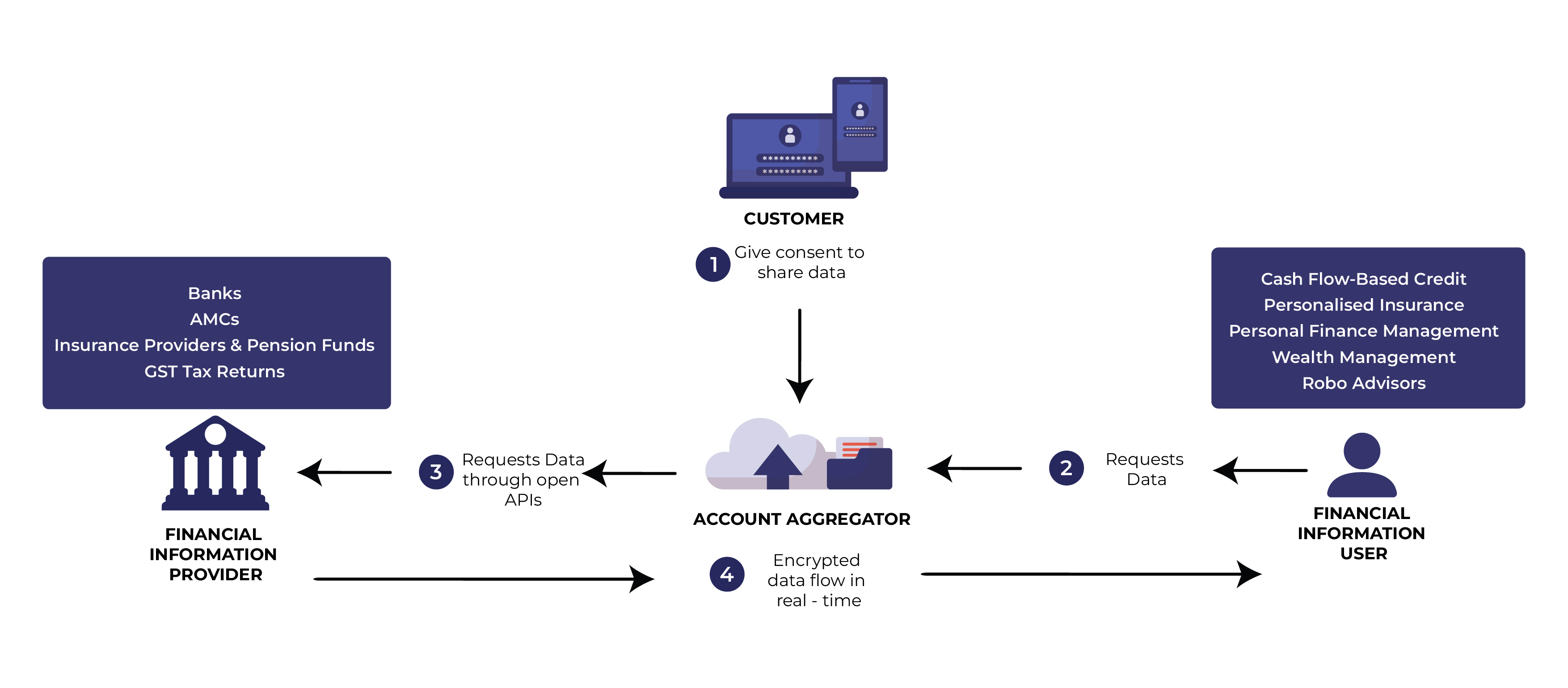

Account aggregation or financial data aggregation is a technique used in the financial services

industry involving the collection, gathering, and synthesis of information in one place from

multiple financial accounts, such as loan accounts, savings and current accounts, credit cards,

investment accounts like mutual funds and demat accounts, public provident fund, income tax

returns, as well as supplementary business or consumer accounts in e-commerce, food or cab

aggregators. The data collection, assembling, and sharing are enabled via open application

programming interface (API) connections.

The inception of the Account Aggregator framework in India dates back to 2016 when the

Reserve Bank of India held joint consultations at the Financial Stability and Development

Council (FSDC) with representation from RBI, SEBI, IRDAI, and PFRDA and released the Master

Guidelines for the framework. That’s how a new class of NBFCs known as Account Aggregators

(AA) was conceptualized. In 2021, the AA ecosystem saw the light of day with eight large private

sector banks joining it.

The AA framework empowers citizens to share data only with their explicit electronic consent, in real time, directly from FIPs to FIUs. Data cannot be shared or misused without consent. AAs cannot view, process, or store the data—they act only as secure pipes for data transfer and consent management.

The process works as follows:

Currently, a customer needs to sign up with multiple Account Aggregators to complete transactions. This increases operational efforts for institutions as they need to access customer data from various sources by integrating with each data provider. To significantly reduce this operational burden, AAs plans to introduce interoperability, eliminating the need for individuals to open accounts with multiple aggregators, which in turn, will allow banks, NBFCs, and other financial institutions to exchange customer data seamlessly.

Sahamati, an industry body within the Account Aggregator ecosystem, is running a pilot program to test interoperability. If interoperability kicks in, customers’ financial data can be accessed across different financial institutions even if those institutions are linked to different aggregators, once a customer has given consent through any AA.

The views in this blog are those of the author and do not necessarily reflect the views of Vivriti. This article is for general information only and is not legal or investment advice.

Copyright © 2023 Vivriti Capital. All Rights Reserved

Under Construction

Please fill in the details

to cancel the NACH mandate

Please fill in the details to cancel the NACH mandate

Ms Namrata Kaul brings on board over 30 years of global banking experience. She has served as the Managing Director, Corporate and Investment Banking at Deutsche Bank AG. Prior to that she was Head of Asia Business for Deutsche Bank based out of London, involved in multi country interface. Ms Kaul has been involved in developing the strategy roadmap for Deutsche Bank India as part of the India Board and was instrumental in defining and executing the Asia Focus strategy for the EMEA business. She was the founder of Deutsche Bank's Diversity initiative in India. Ms Kaul had earlier worked with ANZ Grindlays Bank in various leadership roles across Treasury, Corporate Banking, Debt Capital Market and Corporate Finance in India and the UK.

Ms Kaul serves on the Board of CARE International. She is a Management Postgraduate from IIM Ahmedabad and has completed a Chevening scholarship on Leadership from London School of Economics.